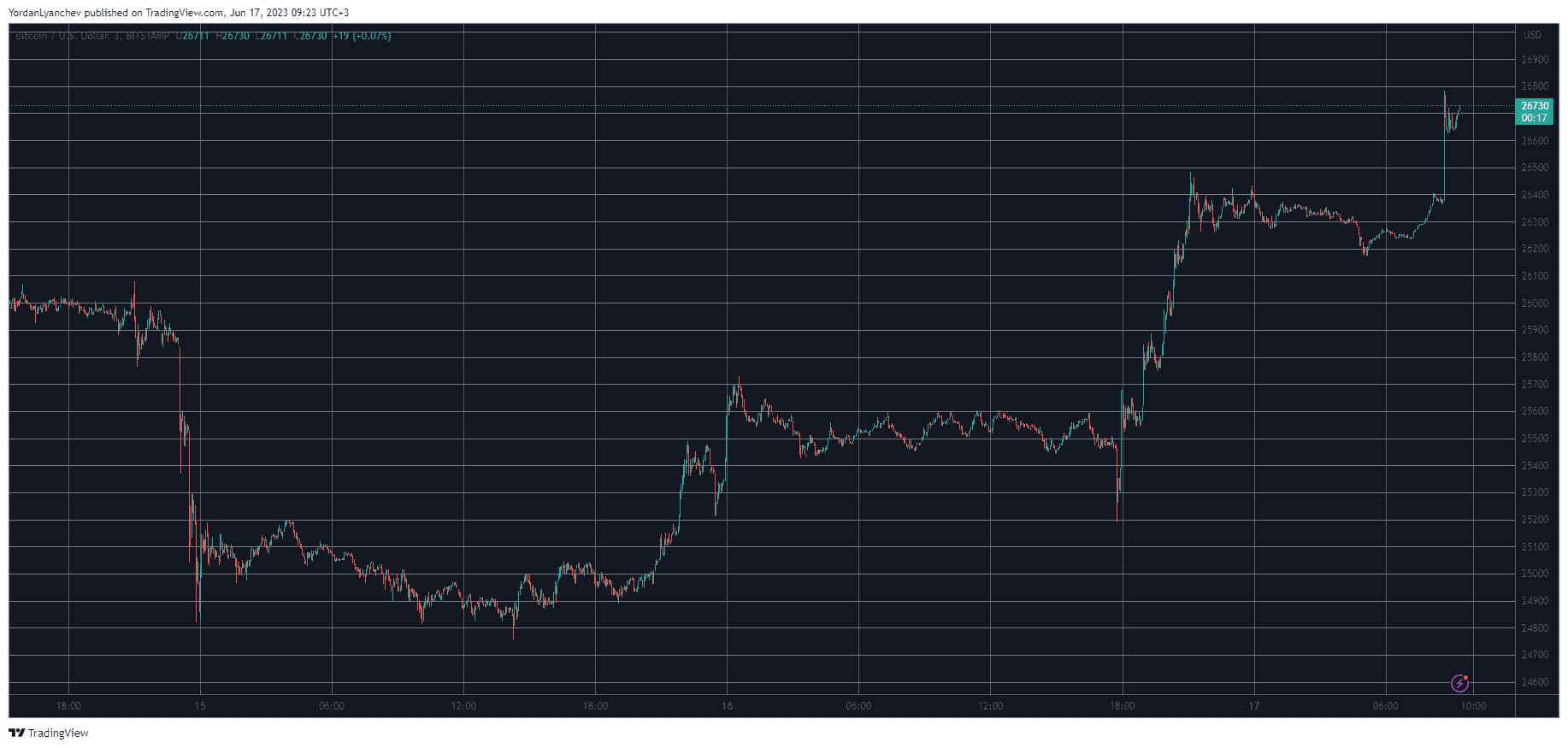

After several days of depressing price movements, bitcoin finally went on the offensive and shot up by almost $2,000 in the past 24 hours to register its highest price tag since June 8.

Expectedly, this has resulted in millions of dollars worth of liquidations, with short positions representing almost 80%.

- Following the SEC’s lawsuits against the two largest crypto exchanges – Binance and Coinbase – as well as the CPI numbers from Wednesday and the Fed’s pivot from its interest rate hiking policy, bitcoin’s price performance was quite underwhelming.

- The asset recently charted its lowest price tag in three months. The altcoins, though, suffered even more, and the total crypto market cap had declined by $130 billion within less than two weeks at one point.

- However, the bulls finally have a cause for celebration. The past 24-48 hours have been significantly more beneficial for the entire market.

- BTC had recovered some ground and stood at $25,500 after BlackRock’s filing for a Bitcoin Spot ETF. After a minor setback yesterday and a dip to $25,200, the cryptocurrency went on a tear and skyrocketed to a 9-day high at $26,800.

- Needless to say, most altcoins have mimicked or even outperformed BTC on a daily scale, with Solana, Polygon, Ethereum, Aptos, and Algorand jumping by up to 9%. QNT has soared the most from the larger-cap alts, following a 20% surge.

- This has harmed mostly short traders. The total value of liquidated positions stands at over $90 million on a 24-hour scale, while short traders are responsible for more than $70 million (approximately 80%).

- Bitcoin and Ethereum have the largest share of the pie, with almost $50 million out of the entire $90 million, according to Coinglass.

{kind=link}

The post Almost $100 Million in Liquidations as Bitcoin (BTC) Soared to Weekly High appeared first on CryptoPotato.